.jpg)

Tax Alert: Key Changes to Indonesia’s MSME Final Income Tax Framework

Tax Alert: Key Changes to Indonesia’s MSME Final Income Tax Framework

The Government of Indonesia has issued Government Regulation No. 20 of 2026 (PP 20/2026) regarding the amendment to Government Regulation No. 55 of 2022 (PP 55/2022) concerning the adjustment of arrangements in the field of Income Tax. The regulation became effective on 22 April 2026 and significantly modifies the eligibility criteria for the 0.5% MSME Final Income Tax framework previously established under PP 55/2022.

PP 20/2026 is intended to ensure that the MSME Final Income Tax facility is better targeted, equitable, sustainable, and applied with high fiscal integrity. External materials from the Directorate General of Taxes (DJP) indicate that the updated framework reflects an aggressive response to tax avoidance, focusing on eliminating corporate tax planning strategies such as "firm-splitting" (fragmenting a single business into multiple corporate shells) and "bunching" (intentionally holding back or suppressing reported revenue). Furthermore, the regulation explicitly integrates international tax standards to fulfill commitments linked to Indonesia's ongoing OECD accession process.

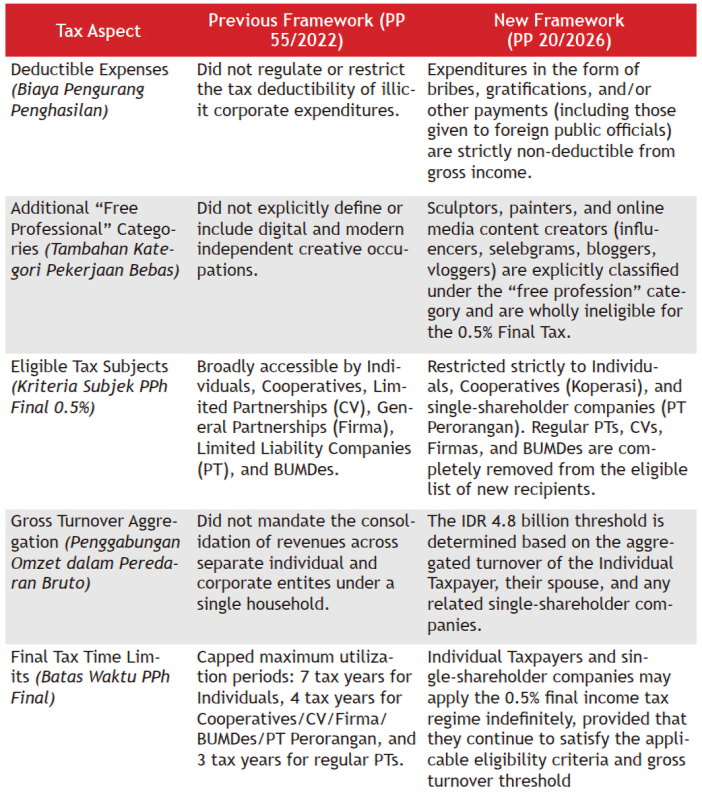

For small business owners, PP 20/2026 maintains the core 0.5% preferential tax rate and the IDR 4.8 billion annual gross turnover ceiling completely unchanged. The narrative circulating within the business community stating that small business tax rates have automatically spiked to a flat 22% on gross revenue is entirely incorrect; disqualified entities simply transition to the general income tax regime where tax is levied on net profit (laba usaha), not revenue. However, corporate entities such as Limited Partnerships (CV), General Partnerships (Firma), regular Limited Liability Companies (PT), and Village-Owned Enterprises (BUMDes/BUMDesma) are no longer permitted to access this facility as new beneficiaries.

For individual taxpayers and single-shareholder companies, the regulation introduces strict exclusions for services relating to free professions (pekerjaan bebas). The list of excluded free professions has been heavily modernized and aligned with PMK 168/2023 to encompass technical experts (lawyers, accountants, architects, doctors, consultants, notaries, PPAT, appraisers, actuaries), educators (trainers, coaches, teachers, preachers, moderators), and digital economy creative workers (influencers, bloggers, vloggers, content creators, and online media digital artists). If a specialized individual registers a single-shareholder company to deliver professional services matching their expertise, that entity is barred from utilizing the 0.5% final tax.

Furthermore, the calculation of the IDR 4.8 billion threshold is now applied comprehensively. The turnover calculation shifts to look at the global economic footprint, aggregating standard business revenue, free profession income, other final taxes, and foreign-sourced income. Additionally, the aggregation rules for married couples are absolute. The turnover of both spouses, along with minor children and all single-person companies established by either party, must be fully consolidated even if they hold a written prenuptial agreement for separate assets or utilize separate tax identification numbers (NPWP).

For corporate taxpayers (CV, Firma, regular PT, and BUMDes/BUMDesma) that have actively utilized the incentive prior to the enactment of PP 20/2026, the regulation allows them to fully run out their pre-existing legal duration granted under PP 55/2022. This means a remaining duration from their initial year of registration can be consumed without immediate retroactive cancellation. Existing tax exemption certificates (Surat Keterangan) held by individual, single-shareholder company, or cooperative taxpayers remain valid until the respective transitional relief periods conclude or the criteria are formally breached.

BDO can assist taxpayers in assessing their eligibility for the MSME Final Income Tax under PP 20/2026, executing comprehensive global revenue aggregation reviews, analyzing transitional grandfathering windows for corporate groups, and structuring robust accounting and bookkeeping transition strategies.

For further information, please contact our team at corsec.helpdesk@bdo.co.id

PP 20/2026 is intended to ensure that the MSME Final Income Tax facility is better targeted, equitable, sustainable, and applied with high fiscal integrity. External materials from the Directorate General of Taxes (DJP) indicate that the updated framework reflects an aggressive response to tax avoidance, focusing on eliminating corporate tax planning strategies such as "firm-splitting" (fragmenting a single business into multiple corporate shells) and "bunching" (intentionally holding back or suppressing reported revenue). Furthermore, the regulation explicitly integrates international tax standards to fulfill commitments linked to Indonesia's ongoing OECD accession process.

Key Highlights

The following comparative matrix outlines the structural shifts introduced under PP 20/2026 relative to the previous framework of PP 55/2022:

What Taxpayers Should Note

For small business owners, PP 20/2026 maintains the core 0.5% preferential tax rate and the IDR 4.8 billion annual gross turnover ceiling completely unchanged. The narrative circulating within the business community stating that small business tax rates have automatically spiked to a flat 22% on gross revenue is entirely incorrect; disqualified entities simply transition to the general income tax regime where tax is levied on net profit (laba usaha), not revenue. However, corporate entities such as Limited Partnerships (CV), General Partnerships (Firma), regular Limited Liability Companies (PT), and Village-Owned Enterprises (BUMDes/BUMDesma) are no longer permitted to access this facility as new beneficiaries.For individual taxpayers and single-shareholder companies, the regulation introduces strict exclusions for services relating to free professions (pekerjaan bebas). The list of excluded free professions has been heavily modernized and aligned with PMK 168/2023 to encompass technical experts (lawyers, accountants, architects, doctors, consultants, notaries, PPAT, appraisers, actuaries), educators (trainers, coaches, teachers, preachers, moderators), and digital economy creative workers (influencers, bloggers, vloggers, content creators, and online media digital artists). If a specialized individual registers a single-shareholder company to deliver professional services matching their expertise, that entity is barred from utilizing the 0.5% final tax.

Furthermore, the calculation of the IDR 4.8 billion threshold is now applied comprehensively. The turnover calculation shifts to look at the global economic footprint, aggregating standard business revenue, free profession income, other final taxes, and foreign-sourced income. Additionally, the aggregation rules for married couples are absolute. The turnover of both spouses, along with minor children and all single-person companies established by either party, must be fully consolidated even if they hold a written prenuptial agreement for separate assets or utilize separate tax identification numbers (NPWP).

Transitional Provisions

PP 20/2026 provides distinct transitional treatments to prevent immediate financial disruption for active taxpayers. For Individual Taxpayers whose tax incentives under the previous PP 55/2022 framework expired in Fiscal Year 2024 or 2025, they are legally permitted to continue using the 0.5% Final Tax for Tax Year 2025 and 2026, or Tax Year 2026 respectively, provided they meet standard criteria. Similarly, Single-Shareholder Companies whose incentives expire in Fiscal Year 2025 may continue to utilize the facility through the end of Tax Year 2026. Registered Cooperatives whose incentives expire between Fiscal Years 2024 and 2029 receive an extended window, allowing them to utilize the final tax through Tax Year 2029.For corporate taxpayers (CV, Firma, regular PT, and BUMDes/BUMDesma) that have actively utilized the incentive prior to the enactment of PP 20/2026, the regulation allows them to fully run out their pre-existing legal duration granted under PP 55/2022. This means a remaining duration from their initial year of registration can be consumed without immediate retroactive cancellation. Existing tax exemption certificates (Surat Keterangan) held by individual, single-shareholder company, or cooperative taxpayers remain valid until the respective transitional relief periods conclude or the criteria are formally breached.

Recommended Actions

Taxpayers planning to evaluate or adjust their MSME tax standing should consider taking the following steps:- Review eligibility status under the heavily restricted taxpayer and corporate entity criteria.

- Evaluate combined spousal, family, and minor children revenues to assess compliance with the IDR 4.8 billion aggregate threshold.

- Audit cross-entity corporate groupings to map out potential exposure to "firm-splitting" aggregation rules.

- Identify the precise remaining utilization timelines and expiration dates for active CVs, Firmas, or regular PTs.

- Implement proper financial accounting and bookkeeping infrastructure to measure net taxable profits in preparation for the general tax regime.

- Review corporate compliance guidelines

BDO can assist taxpayers in assessing their eligibility for the MSME Final Income Tax under PP 20/2026, executing comprehensive global revenue aggregation reviews, analyzing transitional grandfathering windows for corporate groups, and structuring robust accounting and bookkeeping transition strategies.

For further information, please contact our team at corsec.helpdesk@bdo.co.id